My Private key was compromised.

This is where I originally posted all my research & investment thesis:

Hence, I’m re-uploading all my writings to this account.

Please subscribe to this new account and support me in my research.

This research was originally posted on November 13, 2022.

NOTE: This is NOT investment advice. This primer series should only be used as a reference to understand the working of different DeFi lending & borrowing operational models.

In case you missed it: Primer Series Part 1: Intro to Lending & Borrowing Mechanics

Deep Dive: CDMs & CDPs

Part 2 of this primer focuses on two primary operating models used by borrowing and lending projects.

CDMs vs. CDPs

CDMs vs. CDPs

(Over) Collateralized:

-

Debt Markets: where the DeFi protocol has both borrowing and lending capabilities (two-sided credit market), and

-

Debt Positions: where the DeFi protocol only allows users to borrow crypto assets (one-sided credit market).

This primer will focus initially on a brief overview of each model and then I provide an in-depth case study on Compound, Aave, and Maker.

Collateral Debt Markets (Compound and Aave)

Collateralized debt markets (CDMs) are DeFi platforms that provide two-sided credit markets via lending pools, essentially a smart contract used to coordinate borrowing and lending among market participants.

The borrowing process for CDMs: a borrower with sufficient collateral submits a loan request with borrowing parameters. When all parameters are confirmed, the loan is executed.

Liquidity Inflow & Outflow

Liquidity Inflow & Outflow

As shown in the figure above, lenders can deposit crypto assets and earn interest income to provide liquidity. Borrowers can deposit collateral in exchange for borrowing & withdrawing a different crypto asset.

Within the lending side, a market for each approved crypto asset creates a liquidity pool, and deposit rates are algorithmically calculated based on supply and demand for the asset.

For example, the interest rate for a particular crypto will increase as:

-

the supply of the asset decreases (lesser deposits) and/or

-

the demand for the asset increases (more borrowings),

and vice versa.

CDMs can also be termed autonomous money markets that reduce the friction often associated with traditional debt markets linked to negotiating interest rates and additional loan terms.

Case Study on Compound— A Collateralized Debt Market Protocol

Transaction Overview

Once a lender’s wallet is connected to the Compound application (link here), the transaction process works as follows:

The same process can be noticed in AAVE with 'aTokens'

The same process can be noticed in AAVE with 'aTokens'

-

A lender deposits ETH into the ETH pool, which is then available for other users to borrow at a variable rate.

-

The lender receives a cETH

-

To close the position, the lender then exchanges cETH back into the protocol to recoup both the principal deposit and accrued interest.

Note: ‘cETH’ is an interest-bearing ERC-20 token used to record ownership within a given market.

On the borrowing side, a user must supply cETH as collateral to borrow USDC from the lending pool. Thus, the process works as follows:

A borrower has multiple choices as to which crypto they can borrow depending on the collateralization ratio

A borrower has multiple choices as to which crypto they can borrow depending on the collateralization ratio

-

The borrower must first deposit ETH into the lending pool.

-

The borrower simultaneously mints a proportionate amount of cETH.

-

The borrower then deposits the cETH as collateral for a loan.

-

At this point,

-

the borrower withdraws USDC from the lending pool based on the collateralization ratio specified.

-

Interest payments are then automatically added to the borrower’s outstanding debt balance, which is paid when the borrower wants to retrieve the ETH deposited by them as collateral.

-

-

To close the loan at any time, the borrower repays the outstanding ‘USDC + Interest‘, which unlocks the collateral.

-

Each deposit is assigned a collateralization ratio, and more volatile cryptocurrencies have higher collateralization requirements.

-

If the loan becomes under-collateralized (i.e. if the value of the ETH falls below the predetermined threshold ) and the borrower does not quickly top up the collateral, the position is liquidated directly on the open market at the current market price to fund the outstanding debt balance.

-

What are cTokens?

After supplying crypto into the pool, a lender automatically receives ‘cTokens’, which are ERC-20 tokens representing the type and amount of assets deposited. There is a different type of cToken for each market, such as ‘cETH’ for ETH or ‘cDAI’ for DAI.

Each cToken can be viewed as proof of a deposit that essentially tokenizes the user’s ownership stake within a given liquidity pool based on the proportion of funds added relative to the total supply.

As mentioned before, rather than receiving periodic interest payments, interest income automatically accrues to a lender through the variable exchange rate between cTokens and the underlying crypto asset.

The number of cTokens owned by a user doesn’t change. Still, each token becomes convertible into a more significant amount of the underlying pool of assets as borrowers pay interest. A lender can withdraw funds from the pool at any point by converting cTokens back into the underlying asset at an exchange rate that increases or decreases over time as borrowers pay interest back into the platform. This is the mechanism by which interest income is distributed to lenders.

For instance:

Let’s assume there are 50 ETH in the ETH pool and 2500 cETH in circulation. I deposit 20 ETH (total of 70 ETH) into the pool and receive 1000 cETH at the current exchange rate (i.e., ~50 cETH/ETH).

After I deposit the ETH, the protocol automatically mints the number of cETH needed to reflect my ownership (i.e., ~28% = 1000 cETH/3500 cETH) of the ETH pool.

Over the next few months, there are no new deposits, but borrowers pay 3 ETH in total interest payments to the lending pool.

As a result, the ETH market consists of 73 ETH but there are still 3000 cETH outstanding, so the new exchange rate is 41.1 cETH/ETH.

Thus, now I own 1000 cETH, which can be redeemed for ~24.33 ETH.

The primary benefit of cTokens is improved capital efficiency and market liquidity.

I, as a lender, can earn interest income while simultaneously deploying cTokens across other DeFi applications, such as decentralized exchanges or other lending protocols. This means that in addition to earning a yield on the deposited crypto assets, I can also use cTokens to further participate in DeFi protocols, such as providing liquidity to a DEX or engaging further with other lending & borrowing protocols.

Rather than paying a transaction fee for each periodic interest payment, borrowers & lenders are only required to pay transaction fees when opening or closing a position. From the protocol’s perspective, interest payments are also retained within the lending pool rather than being immediately distributed to user wallets, which improves market liquidity.

FAQ

Can lenders simply buy more cTokens to increase the interest they earn? No, cTokens cannot be purchased on an open market as cTokens can only be minted and held by lenders as long as they provide liquidity to the shared pool of that particular crypto asset.

How will borrowers and lenders benefit? Borrowers receive interest income from cTokens that can be converted to the underlying crypto asset. Lenders turn their unique insights on borrowers into direct profits by receiving cTokens that they can convert to the underlying crypto asset. Also, by minting cTokens, lenders:

earn interest through the cToken’s exchange rate, which increases in value relative to the underlying asset, and

gain the ability to use cTokens as collateral.

How does this relate to lending/borrowing on other decentralized lending platforms? *cTokens represent assets in a loan that are supplied by the lenders. Based on the borrowers' ability to repay the loan, lenders are rewarded for their deposits as such borrowers and lenders do not directly compete with each other.

Interest Rates Support Market Liquidity and Stability

Since Compound lends collateral assets to borrowers, lenders assume liquidity risk when supplying capital to a lending pool (also referred to as protocol risk), essentially the inability to withdraw the principal deposit amount and/or interest income.

Unlike traditional credit markets where there are intermediaries such as banks, rating agencies, and so forth to hedge liquidity risk, Compound or any other DeFi protocol does not establish these hierarchies. This lack of objective and structured methods for mitigating liquidity risk introduces the potential for unpredictable liquidity events such as bankruptcy and illiquidity.

Compound does not guarantee liquidity to lenders or borrowers, but each lending pool must maintain sufficient liquidity such that assets are available for withdrawal at all times.

Reserves are an easy way for lenders to deposit their crypto assets with attractive interest rates and allow borrowers to create a hedged portfolio from Compound borrowing pools. Since compound does not have direct control over the reserves, so the collateral deposited while borrowing from a pool is designated as safe. This increased efficiency allows users to borrow more and lend more, with borrowers having more liquidity.

The probability of a black swan event would involve a scenario where lenders try to withdraw more funds than are currently available.

From the previous example:

If I was the first lender to deposit 30 ETH into the ETH lending pool and a day later, Ryan pledges collateral in the form of a different crypto asset and withdraws 20 ETH from the lending pool. So now, the lending pool only contains a total of 10 ETH.

I would be unable to withdraw my full deposit until Ryan repays his loan of 20 ETH with interest.

In this context, each lending pool must maintain sufficient liquidity. One great feature of Compound is that its interest rate algorithm is designed to incentivize a healthy market liquidity level. Therefore, a ‘bank run’ event is improbable.

The interest rates for both borrowing & lending are primarily driven by the utilization rate (i.e., the percentage of deposits on the platform that has already been lent out) within each market (i.e., borrowing demand compared to total supply).

As the liquidity for a particular crypto asset in the market decreases (& utilization rates increase), the platform automatically increases the lending and borrowing interest rates, incentivizing users to lend crypto assets and repay outstanding debt + interest.

Conversely, during periods of high liquidity (and low utilization rates), the platform automatically decreases interest rates such that lenders are encouraged to withdraw deposits or borrow other crypto assets.

According to Compound’s whitepaper, this formula describes the platform’s borrowing and lending interest rates.

-

Borrowing Rate = Base Rate + (Utilization Ratio * Multiplier)

-

Lending Rate = (Borrow Rate * Utilization Ratio) x (1 - Reserve Factor)

-

Utilization Ratio = Borrowed Assets / Supplied Assets

The loans on any CDM protocol are always overcollateralized, and so is the case with the loans borrowed on Compound. Hence, there’s very little probability that the utilization rates exceed 100% because borrowers always have sufficient interest income to fund the lending rate. While market conditions influence utilization rates, the remaining interest rate parameters are determined by Compound Governance, including:

-

Base Rate: Minimum borrowing rate assuming there is no demand for the asset.

-

Multiplier: Expected change in utilization levels.

-

Reserve Factor: % of the interest on borrowed funds held by the protocol.

Rather than allocating the entire interest payment to lenders, Compound collects a part of the revenue in an insurance pool to cover any future defaults.

For example, a borrower’s collateral may be insufficient to fund their outstanding debt if a loan becomes under-collateralized due to an extreme and sudden price movement. In this scenario, lenders are repaid using the assets from the reserve pool.

Another great example of a CDM protocol is AAVE. I have already briefly written about it here: How is SavingBlocks Optimizing DeFi in its Business Model

Aave: A CDM Lending & Borrowing Protocol

Quick Points:

-

Aave, built on top of the Ethereum blockchain, is a DeFi lending protocol that allows users to lend or borrow crypto assets via liquidity pools.

-

Aave has a governance token called Aave which allows holders to vote on governance issues of the protocol.

-

Lenders deposit cryptocurrencies into liquidity pools and earn interest on the cryptocurrencies.

-

Meanwhile, borrowers deposit cryptocurrencies as collateral to receive a loan in another cryptocurrency.

-

Aave currently has liquidity pools for over 15 ETH-based assets such as USDT, DAI, USDC, GUSD, LINK, BAT, UNI, and much more.

Similar to Compound, when a user deposits their crypto assets into any of the Aave liquidity pools, the lender receives “aTokens” (similar to the cTokens) in exchange.

For example, if the user deposits 100 ETH tokens into the Aave liquidity pool, the user receives 100 aETH tokens that can be exchanged for the underlying collateral. As an ‘aToken’ holder, the lender receives interest. If there is more borrower demand for that token than lenders’ supply, then interest rates would move higher and vice versa.

The holders of AAVE (the native cryptocurrency of the protocol) also benefit from not being charged a fee when taking out a loan denominated in Aave and borrowers that post Aave as collateral get a discount on fees.

Aave offers several new features, including:

-

Multiple lending pools Aave supports multiple lending pools. Each pool consists of its own collection of tokens with independent interest rates and liquidity levels, which helps the protocol mitigate potential contagion risks.

-

For example, the Ethereum AMM Liquidity Pool was the first liquidity pool launched on Aave and allows Uniswap or Balancer liquidity providers to deploy “LP tokens” as collateral.

-

The interest rates and other market dynamics within the AMM Liquidity Pool are separate from other pools on Aave.

-

-

More stable borrowing rates: Risk-averse users can borrow funds from Aave’s lending pools at a more stable interest rate. Importantly, these rates are regular (not fixed) as the protocol may adjust the borrowing rate given extreme market conditions, and lending rates are continuously variable.

-

Credit delegation: One offering on the Aave platform allows a lender to extend an unsecured loan to a known counterparty. The lender takes the credit risk, dictates which borrowers are eligible for participation, and sets the terms of the loan using a smart contract.

-

For instance, Edouard can deposit an approved crypto asset into the Aave Protocol in exchange for ‘aTokens’.

-

But instead of designating the aTokens as collateral to receive a loan, Edouard can set up a Credit Delegation Vault (CDV) and earn additional interest by “delegating” a line of credit to Diego with predetermined loan terms such as the borrowing limit and interest rate.

-

Once delegated, Diego can use Edouard’s assets as collateral to withdraw funds from Aave.

-

Since Diego does not deposit collateral, Edouard cannot enforce repayment, and the loan is therefore backed by trust.

-

-

Flashloans: An unsecured loan where the borrower receives and repays the loan in a single, multi-step transaction. In most cases, Flash loans are typically used to execute arbitrage transactions, refinance debt positions, and optimize returns across various dapps. But in general, Flash loans represent a three-act play: 1) receive a loan, 2) do something quickly with the loan, and 3) repay the loan.

In Aave, borrowers with no collateral can take a flash loan. In a flash loan, the smart contracts have rules that the borrower must pay back the loan (with a small fee of ~0.09%) before the transaction ends, or else the smart contract will reverse the transaction as if the flash loan never happened in the first place. As a result, neither Aave nor the user takes any risk.

Flash Loans Use Cases

Users that take out a cryptocurrency flash loan can use it to buy an asset, sell the cryptocurrency, and then return the original amount in the same transaction while pocketing the profit.

Use cases for flash loans include arbitrage and debt refinancing.

Arbitrageurs can use flash loans to take advantage of price differences between markets to make a profit without putting up any collateral. Meanwhile, borrowers can use flash loans to take advantage of differences in lending rates on various lending protocols.

For example:

Suppose the borrower has an existing loan at Compound with a 10% interest rate but wants to refinance the debt at Cream or Notional Finance, which offers a 5% interest rate.

In that case, the user can take out a flash loan and repay the loan in lending protocol A and then borrow at lending protocol B at 5%. After receiving the proceeds from lending protocol B, the user can pay off the flash loan at Aave.

This flash loan occurs within the time it takes for an Ethereum block to be added to the chain, which is about every 15 seconds.

It is also worth noting the AAVE protocol recently launched a new upgrade, Aave V3, which includes new features, including cross-chain interoperability, improved capital efficiency, and new risk management capabilities. In January 2022, Aaave released Aave Arc for institutional investors.

Aave Arc (Aave Request for Comments)

-

Aave’s product for institutional investors to address security, fraud, and money laundering risks in the DeFi ecosystem creating new lending and borrowing pools exclusively for institutional investors.

-

Strict KYC procedures need to be followed, both on the borrowing side as well as the lending side. Furthermore, Aave implements anti-money laundering and antifraud compliance through an established third-party service provider.

-

These measures enhance risk mitigations for institutional investors and lead to a positive feedback loop with higher institutional participation in these exclusive liquidity pools. The platform supports bitcoin, ether, Aave, and USDC.

(Over) Collateralized Debt Positions (CDPs)

CDPs are lending platforms that offer (over)collateralized loans via a single-sided marketplace. The borrower’s experience is similar to CDMs such as Compound or Aave.

The user deposits a cryptocurrency as collateral in exchange for a different crypto coin. But the back-end tech is designed differently. A CDP-based system does not create an AMM (autonomous money market) but is based on the economic design of a decentralized stablecoin.

Playing with Analogies

CDMs act like banks: where cash by depositors is lent out to borrowers,

CDPs deposited funds are locked in a vault to backstop the issuance of a newly minted stablecoin (e.g., DAI).

These fresh stablecoins are then provided to the borrower as an overcollateralized loan, with the protocol setting an interest rate.

In order to get the initial deposit/collateral back, the user must repay the loan with interest in full.

By periodically changing the interest rate, the protocol ensures the proper flow of funds to maintain the stablecoin (e.g., DAI) peg at $1.

As you can see below, a borrower can draw liquidity in the form of newly minted tokens (usually stablecoins) without relying on other market participants.

CDPs only provide borrowing capabilities.

CDPs only provide borrowing capabilities.

Case Study: Maker

The value proposition for the borrower is the ability to maintain exposure to collateral assets while improving liquidity with DAI, which can be sold for cash or deployed across DeFi applications.

Rather than lending the deposits themselves, Maker locks the collateral in a smart contract and leverages its borrowing and saving products to support the growth and stability of the DAI stablecoin.

Transaction Overview

A user can access the Maker protocol through the Oasis app.

Once a wallet is connected to Oasis, the borrowing process works as follows:

-

The user deposits ETH into a “vault”, which is a smart contract that locks the collateral and records the $$ value of the deposit.

-

The user then receives DAI based on the specified collateralization ratio. Put another way, the borrower receives an overcollateralized loan in DAI that must be repaid in the future.

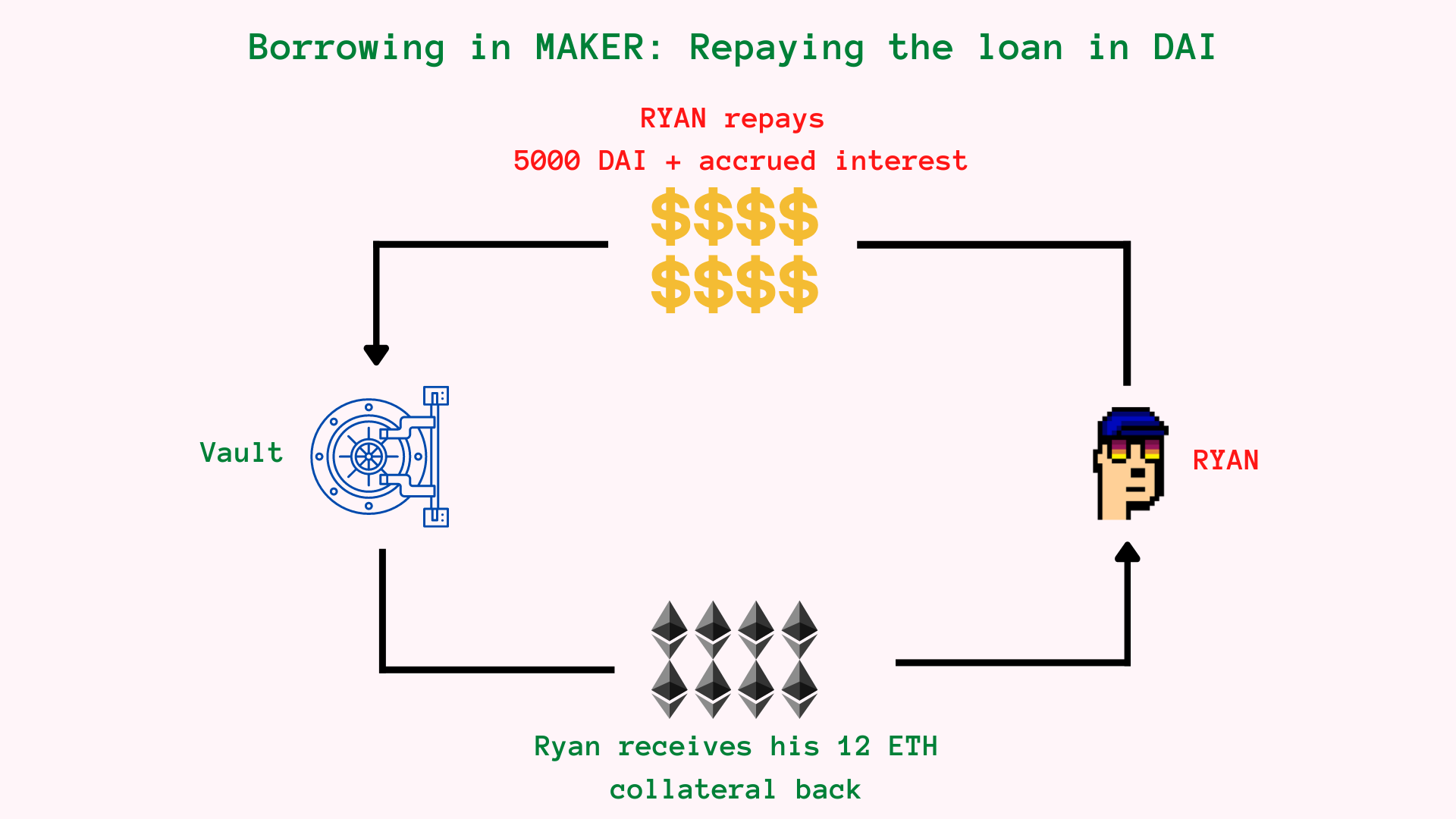

-

The borrower repays the outstanding debt (initial amount + accrued interest) in DAI to unlock the previously deposited collateral, i.e., ETH.

For example

Suppose Ryan deposits 12 ETH into a Maker vault with a collateralization ratio of 300%.

As of today (12 Nov 2022), 1 ETH is worth ~$1200; Ryan deposited ~$15,264 worth of ETH, which allows him to mint up to ~8900 DAI.

But Ryan is bright and mints less than the maximum limit to provide a buffer before a potential margin call in the event that he gets liquidated. So, Ryan mints ~5000 DAI.

Ryan's liquidation price for the loan of 5000 DAI is $728.

If he had borrowed 8000 DAI with a collateralization ratio of 190%, his loan’s liquidation price would have been $1,122.

So the buffer of ~$372 gives him more time to capitalize on his investments with the loan. There’s also a liquidation penalty invoiced directly to incentivize vault owners to avoid liquidation. This penalty fluctuates with the overall debt of the vault.

Interest payments then subsequently accrue on Ryan’s loan based on a variable interest rate, which is actively managed by Maker governance to drive the price of DAI toward its peg (vs. Compound, where interest rates are determined by supply and demand).

And rather than paying interest periodically over a predetermined term, Ryan can close the debt position at any point by repaying the principal + accrued interest.

Maker’s DAI & How the Platform Maintains Its Peg

How is a one-sided credit marketplace more successful & profitable than a two-sided credit marketplace such as Compound or Aave?

There are two primary factors responsible for the success of the Maker protocol:

A. Supporting the $1 Peg: Three factors support & maintain the stability of DAI:

-

The DAI savings rate (DSR),

-

Stability fee to maintain the supply of DAI, and

-

A limit on the supply of DAI against the collaterals.

B. (Over) Collateralization: By overcollateralizing the loans within vaults, Maker protocol hedges its loans against the volatile nature of crypto.

Let’s dive into each in more detail.

A. Supporting the $1 Peg

DAI is an ERC-20 token, like many stablecoins that trade on the open market. As we saw with Luna-Terra, all stablecoins are subject to heavy fluctuations around their $1 peg.

Like many stablecoins:

-

the demand for DAI is spread across its activity on various DeFi platforms or just a desire for a DeFi user to hold a comparatively stable (safe haven) asset

-

the borrowing activity predominantly drives the supply

Hence, the Maker Protocol leverages three primary strategies to maintain the dollar peg:

1. Stability Fees

The stability fee manipulates the supply of DAI and, in turn, helps maintain DAI’s $1 peg. This fee ranges between 0.3%-0.75% between various collateral assets.

-

When the demand is low (DAI is trading below $1), Maker’s governance increases the stability rates to incentivize borrowers to repay the debt, reducing the supply of DAI outstanding on the open market and putting upward pressure on the price of DAI.

-

Contrarily, when DAI trades above $1, Maker’s governance decreases stability rates to incentivize market makers to open a Maker vault, which increases the supply of DAI outstanding and puts downward pressure on the price of DAI.

2. DAI Savings Rate (DSR)

The Maker protocol guarantees a stable value for its DAI stablecoin. To make DAI an inflation-resistant currency, it doesn’t rely on central banks or governments to ensure its stability.

Instead, DAI’s stability is assured by providing users with a variable interest rate, DSR, in exchange for depositing DAI into the protocol.

DSR manipulates the demand for DAI as MakerDAO votes on a lower or higher DSR to influence holders to sell or buy DAI on the open market.

DSR is funded with a percentage of borrower interest payments.

Identical to how a bank charges a higher interest rate on loans than what it offers for the customer’s cash deposits, Maker’s protocol inflows must always be greater than the protocol outflows.

Interest Payments >> DAI Savings Rate (DSR).

Maker Protocol’s DSR differs from Compound or Aave’s as it is not a lending contract, and no party on the other end is borrowing the DAI tokens. The purpose of the DSR is to protect the dollar peg of the DAI stablecoin.

3. Collateralization Ratio (CR)

A CR is a debt ceiling constraining the total supply of DAI available for issuance against different collateral assets. If your loan on the vault reaches its liquidation price, the new DAI cannot be minted until outstanding debts are repaid. Maker’s governance adjusts the debt ceiling of various collateral assets to maintain supply based on current demand levels.

B. (Over) Collateralization

Given how volatile the crypto markets have been lately, the value of collateral locked within vaults must exceed the value of debt outstanding (as measured by the total supply of DAI).

Like Compound, MakerDAO loans are therefore over or sufficiently collateralized based on a predetermined collateralization ratio, typically in the 150% to 200% range, depending primarily on the collateral volatility and borrowers’ risk appetite.

If the collateral value falls below the collateralization ratio, the borrower must

-

repay the loan in DAI or

-

deposit additional collateral.

Otherwise, the protocol incentivizes network participants referred to as “keepers” to scan loans eligible for liquidation. A keeper can sell crypto collateral to repay the loan in DAI and close the borrower’s debt position.

In doing so, the keeper earns a “liquidation penalty”, a fee deducted from the borrower’s collateral and calculated as a percentage of outstanding debt (~10% to 15%). After applying the liquidation penalty, the remaining collateral is returned to the borrower.

It is worth noting that keepers tend to be (sometimes) automated bots that constantly monitor open vaults. It is my understanding that MakerDAO currently manages most keepers, but the long-term goal would be to transition toward more community management.

Further, the MakerDAO Treasury assigns a portion of stability fees towards a backup pool to cover future bad debts referred to as “protocol debt”.

For instance, if the value of a borrower’s collateral decreases below the debt outstanding before the liquidation, the position may be closed at a loss such that MakerDAO assumes protocol debt. In this scenario, the protocol uses funds from the reserve pool to fund the DSR.

If the backup pool is inadequate to fund new protocol debt, there are 2 primary solutions:

-

Auctioning newly minted MKR tokens in exchange for DAI stablecoin, which subsequently pays off the protocol debt. Consequently, the value of the MKR token is diluted.

-

Shutting down the protocol to ensure that all DAI holders and vault borrowers adequately receive the net value of assets to which they are entitled. This might only be done in a severe attack or a hack, as we saw with the BNB chain a few weeks ago.

Thoughts & Remarks

L1s are the primary roadmap for the financial applications of web3. Furthermore, the concept of interoperability enables powerful new capabilities to be layered on top of previously developed protocols, creating unique and more complex dApp ecosystems and co-dependent value-creation flows.

Indeed, "protocols" are becoming synonymous with "dApps" in DeFi.

With their open-source nature, dApps are essentially building blocks that can be combined to create robust protocols. This provides an incentive for protocols to innovate continuously and for dApps to increment in complexity rapidly, accelerating the pace of innovation in DeFi.

One potential for the non-linear evolution of DeFi dApps is that communities can leverage other protocols' innovations, which could cause DeFi to evolve faster than other disruptive business models.

Another is that it becomes challenging to pick winners because a protocol could develop a highly useful dApp that is subsequently improved upon by other developers who fork off with incremental advancements that supplant earlier iterations of the protocol.

While this model may make it harder to determine who the winners are, it does optimize the pace of innovation. This may explain the high velocity of improvement we have seen in DeFi. Also, we have regularly seen that the multi-sided platforms have a fundamental disconnect between their needs and the needs of the protocols they employ.

Before the merge, we saw data transmitted across thousands of blockchains with very high costs, gas fees, and network latency. We're collectively spending billions on scaling blockchains, yet individual L1s remain too small for security needs. And blockchains built on top of other chains are not optimized for their network latency. They need to build their network on top of them.

A handful of projects largely dominate the DeFi industry and its coin market capitalization. Because of this centralization (FTX, Celsius, BlockFi, etc.), it has become increasingly tricky to passively observe and evaluate the projects themselves and the changes they propose to the world. DeFi is still very much an ecosystem of beginners. Still, it is becoming expensive to the point where it becomes more reasonable to evaluate and understand the protocols they choose to build.

Most regulated financial infrastructure today still relies on legacy banking infrastructure. This has unfortunate consequences resulting from the separation of systems created by legacy banking:

-

payments (settlement),

-

clearing and settlement (funds to move money), and

-

the custody of funds (assets).

Financial services are siloed and segregated into various parts, and the talk of DeFi is about the current and near-future evolution of smart contracts: a technology that is 5 years old but is in its nascent stage.

Thank you for reading through. I’d appreciate it if you shared this with your friends who would enjoy reading this.

You can contact me here: 0xArhat.